Borrowers Remain Cautiously Optimistic Despite Pending Interest Rate Increases and Higher Market Volatility

LOS ANGELES, CA, 2017-May-09 — /EPR Retail News/ — High investor confidence, attractive equity markets and positive economic indicators have contributed to favorable commercial real estate lending market conditions in Q1 2017, according to the latest research from CBRE.

While the fairly dramatic increase in long-term interest rates that occurred in late Q4 2016 continued into early Q1 2017, its impact on commercial real estate markets has been fairly limited, especially given the more recent decline in Treasury rates.

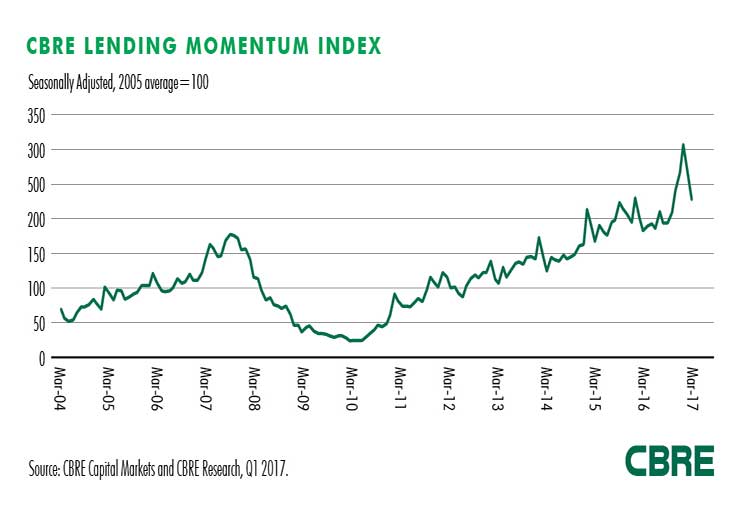

The CBRE Lending Momentum Index, which tracks the pace of U.S. commercial loan closings, fell by 14.3% in Q1 2017 to 228. Despite this decline, March 2017 lending activity was up by a robust 25.2% year-over-year.

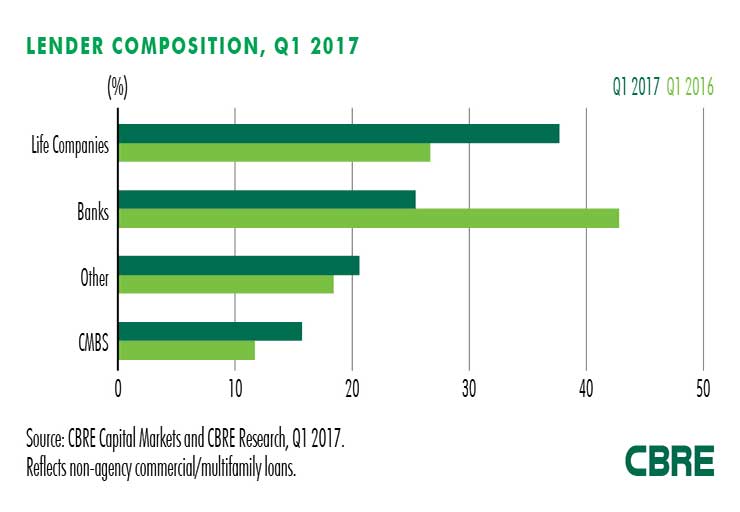

Life companies led all other major lenders in Q1 2017 and increased their share of loans closed by CBRE Capital Markets. They accounted for more than 37% of non-agency commercial loan closings in Q1 2017, up from 34% in Q4 2016, and well above their 27% share recorded in Q1 2016.

While banks maintained their standing as the second most popular lending group in Q1, their market share slipped substantially to 25.5% of loan volume, down from 43% a year earlier. Many key bank interest rates and spreads have not been materially affected by the recent increases in Treasury rates. However, bank construction lending remains limited and banks are selective in granting loans.

“Borrowers generally are optimistic as the U.S. commercial real estate lending market remains favorable despite the Fed’s policy of raising short-term interest rates and the possibility that long-term rates will resume their climb after leveling off in recent weeks. Life company, agency and non-bank lenders are active in the market and have new allocations to place mortgages in 2017. CMBS lenders have successfully tested new risk-retention deal structures with the promise of providing needed liquidity to the marketplace, and private equity funds have raised record amounts of “dry powder” capital to deploy for equity restructuring, new construction and bridge deals. And credit spreads remain tight, allowing borrowers to take advantage of low all-in mortgage rates,” said Brian Stoffers, Global President, Debt & Structured Finance, CBRE Capital Markets.

CMBS lenders have incrementally improved their share of closings over the past year, as the loan pricing environment has become more favorable and issuers have created structures to satisfy risk-retention requirements. However, CMBS continues to lag other major lending groups by a considerable margin. CMBS lenders accounted for 15.8% of non-agency lending volume in Q1, up slightly from their 11.7% share a year earlier.

The “Other” lender category, which includes REITS, private lenders, pension funds and finance companies, continues to play a significant role in providing a variety of bridge, permanent loan and construction financing. They accounted for 20.7% of non-agency volume in Q1, down slightly from 24.1% in Q4 2016.

To request a copy of the Q1 2017 edition of CBRE’s U.S. Lending MarketView Snapshot or to speak with a CBRE expert, please contact Ayana Miller (212.984.6506 or ayana.miller@cbre.com).

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBG), a Fortune 500 and S&P 500 company headquartered in Los Angeles, is the world’s largest commercial real estate services and investment firm (based on 2016 revenue). The company has more than 75,000 employees (excluding affiliates), and serves real estate investors and occupiers through approximately 450 offices (excluding affiliates) worldwide. CBRE offers a broad range of integrated services, including facilities, transaction and project management; property management; investment management; appraisal and valuation; property leasing; strategic consulting; property sales; mortgage services and development services. Please visit our website at www.cbre.com.

MEDIA CONTACT:

Robert McGrath

212.984.8267

robert.mcgrath@cbre.com

SOURCE: CBRE Group, Inc.